When Gaya Arun bought Stadium Market at 33rd Avenue and Main Street in 2021, things were looking up. Retail was riding high. Canada was coming out of pandemic lockdowns, and the worst expectations of economic downturn were avoided with wage subsidies, loans and the Canada Emergency Response Benefit.

But in the three years since, despite national data showing significant growth in profit margins, especially in the food retail sector, she and other independent grocers say they’re facing serious challenges.

While national data show increases in consumer spending on groceries, they say they’re being squeezed between downward pressure on sales and upward pressure on prices from continual hikes at the supplier level.

‘I don’t think I have a future here’

Arun believes Vancouver’s out-of-control real estate is playing a significant role in it. Having an affordable place to live, she notes, gives people space to spend money, but today’s housing market results in ever-reducing expendable income.

“I moved here in the early ’90s, and at that time you could find a place to rent for $1,000, or $800, even $600. $2,500 for one bedroom? It doesn’t matter how much money you make, … I can’t imagine paying $2,500,” Arun says.

“I thought I would live and die here, but I don’t think I have a future here.”

The challenges with rising property values also apply to rent for businesses, she says, noting that because of triple-net leases, she’s responsible not only for paying rent, but for bills and property taxes.

Today, her life is consumed in her work. “I work 364 days a year, and I will wake up, shower, go home, shower, go to sleep, and it’s just getting worse,” Arun says.

“The last three months have been the worst.”

Challenges in Little India

That’s a sentiment shared several blocks southeast at 49th and Fraser, where Tanraj Dhillon’s family operates Garden Fresh in North America’s oldest Little India.

Garden Fresh has been open since 2009, but Dhillon’s dad opened his first Vancouver grocer in the mid-1990s. And the last few months have been the hardest for grocers in the family’s whole time in the business, Dhillon said. That includes during the financial crises of the early 2000s and in 2008.

“This one’s by far the worst,” he said. “The whole country’s going through it right now.”

Because Garden Fresh has been in business for a decade-and-a-half, he said his family is able to weather the storm.

“But I know a lot of stores personally, especially the ones that opened up recently, they’re not doing well,” he said. “It’s a rough year this year.”

Dhillon agrees it’s a symptom of struggling families, who are buying fewer items than they have in the past.

“They just want to buy the bare minimum just to get by. It’s pretty bad, especially in this area. It’s a lot of immigrants and a lot of older folks,” Dhillon said, noting many in the neighbourhood are reliant on pensions or are still getting a foothold in Canada.

National data tells a different story

But while local, independent grocers say they’re struggling — others didn’t comment on record but confirmed they, too, are experiencing hardship in recent months — national data appear positive for the supermarket sector overall, showing large increases in profits in recent years.

In fact, the current troubles facing small grocers follow a few years of significant growth. If the last few months have been some of the hardest for Dhillon’s family, the pandemic proved to be some of the best, he said.

And that is borne out by data from Statistics Canada.

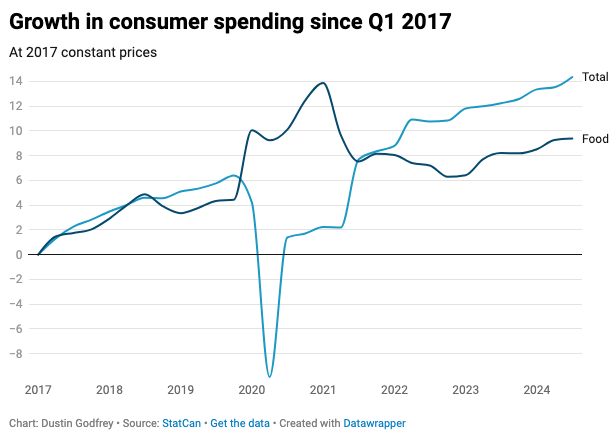

Quarterly GDP data show soaring growth in household spending on food, with quarterly data showing each quarter of 2020 at 6.1% to 8.8% higher than in 2019 after accounting for inflation.

An archived StatCan report notes pandemic restrictions on dining out were likely a significant factor in that growth — in that same year, overall quarterly household spending was down 0.8% to 15%.

That growth in food retail spending came down, and even turned into year-over-year declines between late 2021 to early 2023, before trending more closely with total consumer spending in the last year.

Profits are up — way up

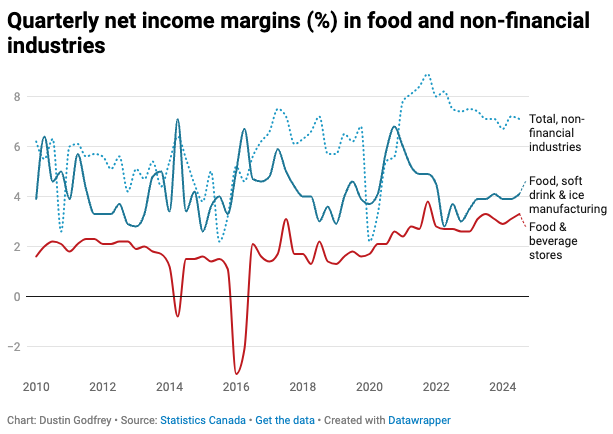

But while sales have moderated since the start of the pandemic, profits haven’t, notes economist Jim Stanford, director of the Centre for Future Work.

“The most recent data confirms food retail profits remain elevated far above pre-pandemic norms,” he said in an emailed statement, citing StatCan data.

Profit margins in food retail tend to be low, even within the broader retail sector, averaging at about 1.5% between 2010 and 2019, compared to 5.5% among all non-financial industries. Return on equity, a measure used to gauge profit not as a proportion of income, but as a proportion of investors’ equity, has been only slightly lower, at 9.8% and 10.0% respectively.

But in the last five years, profit margins and return on equity have soared in the food retail sector in ways they haven’t for other sectors.

Net income margins from 2020 to 2024 have increased nearly 83% compared to the averages for the prior decade, while return on equity since the start of the pandemic has increased 75% compared to 2010-19, according to StatCan.

By comparison, income margins for all non-financial industries increased by a more modest 25.2%, while return on equity increased just 12.6%.

So, why are indie grocers struggling?

For the whole sector, the profits that rocketed up from the beginning of the pandemic haven’t come down, leaving questions about why independent grocers are struggling in the city. And it isn’t just Arun and Garden Fresh — others who didn’t speak on the record also said they were struggling in recent months.

Stanford said their “specific anecdotes don’t necessarily reflect what’s happening in the whole economy.” But he said they may be operating in markets that are experiencing “more challenging trends.”

One of those more challenging trends could be, as Arun has pointed out, the housing market, with Vancouver facing the toughest housing crisis in the country.

Independent grocers like Garden Fresh and Stadium Market are also having to compete with large chains, which Stanford noted have a number of advantages not available to local grocers for absorbing the impacts of inflation.

Inflation may hurt some more than others

While Arun and Dhillon cite inflation as one of their pain points, critics argue large chains have actually benefited from inflation, and they have been in the hot seat over food prices in recent years.

Galen Weston, chair of Loblaw Companies Ltd., has pointed to suppliers as the drivers of inflation. But others suggest Loblaw has been using inflation to pad its profits through what economists call “seller’s inflation.”

University of Massachusetts Amherst economists Isbella Weber and Even Wasner argued last year that seller’s inflation was the primary driver of inflation in the United States.

The pair described a pattern of inflation that starts with the usual supply-and-demand imbalance, but takes off as rising prices effectively give suppliers and retailers an opportunity to take in more profits. This can be due to an outsized market share, and because consumers are already primed for higher prices from existing inflation.

Some politicians and columnists have replaced the term “seller’s inflation” with “greedflation,” often as a way to dismiss the concept. One columnist, Matthew Yglesias, wrote in 2022 that, “only a very stupid person would think companies suddenly became greedy in 2021 after years of being non-greedy.”

This particular take has been countered by others as failing to understand seller’s inflation — that it isn’t a change in greed, but a change in opportunity, in this case, existing inflation being used as a vehicle for increasing profits.

Stanford noted early last year that Loblaw’s arguments that suppliers, not grocers, were driving up costs fell flat when one looked at changes to profits between the two sectors.

Net income margins for manufacturers increased a much more modest 2.6% in 2020-24 compared to the previous 10 years, while return on equity for the sector declined by 8.7%.

Loblaw chief financial officer Richard Dufresne told investors in the fourth-quarter 2021 quarterly earnings call that the company had, so far, “been successful in passing through the inflation” to consumers, and that if inflation “stays at the levels we’re in now, I think we should be able to continue to do it.”

Even as the company has bragged in later earnings calls of price increases below the rate of inflation, “clearly demonstrating the role we are playing to help stabilize food prices for our customers,” the company has assured investors it’s maintaining its profits.

Annual reports filed by Sobeys’ parent company Empire similarly tout the company as a leader in addressing inflation by finding ways to reduce costs.

Control the brand, boost the margins

Many of the mechanisms the big chains point to as cost savings aren’t available to local, independent grocers.

In the Q4 2021 Loblaw earnings call, Dufresne told investors the “merchandising teams are seeing opportunities to get more credit for less investment than we were seeing last year.”

Throughout the last few years, Weston, Dufresne and CEO Per Bank have highlighted the performance of generic brand products, also known as control or private brands, like No Name or President’s Choice. In Q1 2023, Dufresne said generic brand sales grew at “more than twice the rate of national brands.”

And generic brands come with higher margins for retailers — so much so that one former White House economic advisor suggested to The Atlantic’s podcast Good On Paper in October that they may be a big part of the reason for increasing profits for grocers south of the border.

“It’s about penny profit. You want to earn more penny profit when you sell a controlled brand product than you earn when you sell a national brand product,” Weston said in Q1 2022. “And that means the margin needs to be significantly higher. And that’s how the program is engineered.”

When asked by a TD Securities analyst in the Q4 2021 call if there was anything other than control brands the company could point to “in terms of the penetration or profitability that you might be working on,” Weston told investors they “see disproportionate amount of opportunity in control brand.”

But generic brands aren’t an option for independent grocers.

Big chains, big negotiating power

Sobeys’ financial filings hint at a different mechanism: negotiating power.

In annual reports, the company notes that it “continues to focus on supplier relationships and negotiations to ensure competitive pricing for customers,” and that it “continues to be well positioned to pursue long-term growth despite the impacts of global economic uncertainties.”

The negotiating power of large chains puts independent grocers at a disadvantage. That’s a significant pain point for small stores, who often offer lower prices in order to compete with the large chains.

“We have to be lower than everyone else in order to get people. And if we don’t, then we don’t have customers, then we can’t survive,” Arun said.

While Dhillon said he’s able to offer lower prices on produce, his family has to buy milk in large quantities from Superstore because it’s cheaper than buying directly from the supplier.

(Dustin Godfrey)

The Canadian Federation of Independent Grocers raised this issue with the Federal-Provincial-Territorial Working Group on Retail Fees, which issued a report on its findings in 2021.

That report notes that 80% of the market share is divided between five players — three food retailers (Loblaw, Sobeys and Metro) and two general retailers (Walmart and Costco).

“It is alleged that independent grocers are forced to absorb some of the increased costs since suppliers provide larger retailers with hidden discounts and allowances (sometimes at the request of retailers) which are not available to independent retailers,” the report reads, noting the working group was provided evidence of suppliers charging independent grocers more than large chains.

CFIG also told the working group independent grocers aren’t provided the same promotions from suppliers that are provided to large chains, and when there were shortages of products, it was those chains that took priority for suppliers.

And while food manufacturers haven’t increased their profits like supermarkets have, Stanford says consumers “don’t have to take sides in finger-pointing between oligopolistic retailers like Loblaw & oligopolistic processors like Cargill or PepsiCo.”

“Both camps have taken advantage of supply disruptions & consumer desperation to fatten profits amidst deep economic & social crisis,” he wrote on Twitter.

Struggling with supplier price hikes

In fact, Arun and Dhillon both say they’ve struggled with suppliers either raising their prices, or being shut out by large supermarket chains.

Independent grocers, however, get caught in the middle, and Arun says the relationship between suppliers and small grocers has degraded — and the pandemic played a role in that.

During the lockdowns, a lot of costs went up for businesses, she said, and those costs didn’t come down when everything started opening up again.

“There’s no principles or respect. It’s like you come up with some kind of excuse and increase the price and take whatever you can,” she said.

Costs, she said, are no longer about value and what suppliers paid, but about pushing the boundaries of what the market can bear. “Greed is just killing everybody,” she said.

Previously, wholesalers would give plenty of notice to grocers about changes in prices. “Now, there’s no formalities there. Every invoice is a different price,” she said.

She pointed to olive oil, as one example, which she said has more than doubled in cost to her from the wholesaler in the last two years. The increases in prices to her are “not cents anymore; it’s dollars.”

While large grocers can absorb those costs — or even simply negotiate better costs — that’s not something independents can do. This can fuel an ever-growing gap between small grocers and chain supermarkets.

“It’s so stressful to keep up,” Arun said.

Normally we paywall longer stories, but today we’ve made this available to everyone because five readers stepped up to fund it in November. As a reader-funded publication, we rely on people like you contributing to fund these stories.

But these stories aren’t cheap. Most publications in Vancouver are focused on clickbait stories. Producing these high-quality, local stories is expensive. And unlike most other places, we’re over 85% reader-funded, from hundreds of paying subscribers.

It costs less than $2 a week to become a Lookout member, and you get access to our paywalled exclusive local journalism, our archive of stories and you’re helping fund independent journalism that goes beyond clickbait stories and headlines here in Vancouver.